Who needs a book to get through school without going broke anyway? A waste of a good hour's worth of wages I say! Back in the 60s and 70s I not only got through school without taking out a loan, I owned a Mustang and was making mortgage payments by the time I donned the cap and gown! Kids today just need to find their bootstraps and pull themselves up a little bit. Now get off my lawn!

If only it were that simple for today's youth. The fact is that while a university education used to cost roughly the same as what I got when I returned my empties at the end of every semester (not an inconsequential amount admittedly), and then virtually guaranteed you a productive career in your choice of white collar work – those days are long gone. More Money for Beer and Textbooks helps young people sort through the confusing jumble of misinformation about post-secondary education that exists out there today. At a time when student costs are escalating, and certain educational paths are leading right to barista-hood instead of a defined benefit pension plan, it is more important than ever for students to stay out of debt and make their lives a little easier.

In order to show that we didn't slap this thing together over a couple nights of drinking games (although that would've probably been a cool book too) we decided to give everyone a preview of the book we released on Monday. If these facts don't convince you that today's student faces some pretty large obstacles, you're tougher to impress than we are. If you want to make these challenges a little less daunting, take a look through the rest of More Money for Beer and Textbooks. We included everything from student living option comparisons, to resume tips, to why you should try making your own beer! If you wish you had seen something like this when you were eating KD five times a week and going through school, make sure and buy one for a special young person in your life who might benefit from not having to learn everything the hard way.

Without further ado…

Chapter 1 – How Much Will School Cost … and Is It Even Worth It?

Before we get into saving money and how to become an expert on the finer points of beer consumption, we probably should address the number-one question on the minds of students bound for post-secondary education. (It’s also on the minds of their parents.) How much is this going to cost?

We won’t lie to you. Today is not an easy time to be a young person, or the supportive parent of a young person. It seems that not a week goes by without a new study coming out that talks about the record levels of student debt or the rapidly rising costs of tuition. The truth is that it’s extremely difficult to pinpoint exactly how much school will cost for your specific situation. Depending on what sort of post-secondary education you want, where you want to go to school, and what sort of lifestyle you plan to live while studying, the answer to the overall $$$ question varies quite a bit.

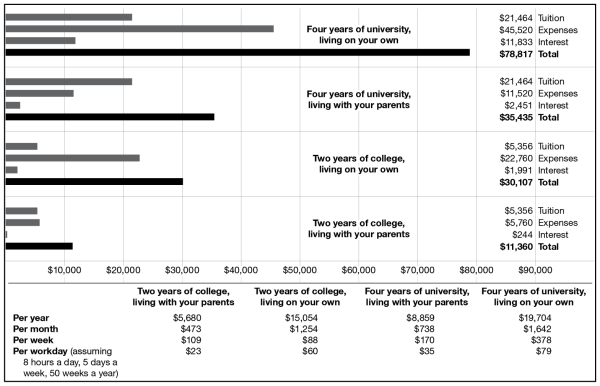

A survey of students across Canada done by RateSupermarket.ca in September 2012 estimates that a student leaving high school today will pay an average total cost of $78,817 for a basic four-year degree if living away from home. Here’s how that breaks down:

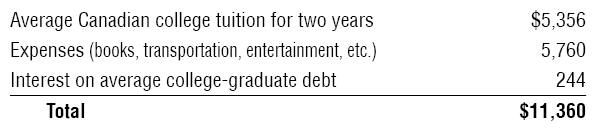

By comparison, here are the averages for two-year college diplomas. First, not living with your parents:

A two-year college diploma if you live with your parents:

The interest was calculated from Canadian average student-debt levels, an average starting income of $39,523 a year (with five percent of it going toward debt repayment), and an extremely optimistic three-percent annual interest rate. You may have noticed that the interest costs are lower for students living at home: this is because the lower cost of living with your parents means that you need to borrow less and therefore can race faster to the end of paying those pesky interest charges. If you’re a little rusty on what interest is and how it works, see the beginning of Chapter 7 for a quick refresher. Also of note: the average university student in Canada these days takes fourteen years to pay off student debt.

While these numbers might surprise parents who have fond memories of their $1,000 tuition and plentiful summer jobs for all who wanted them, they actually weren’t surprising to us recent grads. Moreover, the sizeable difference in overall cost between a college education and a university education presents an interesting cost–benefit scenario to aspiring young Canadians.

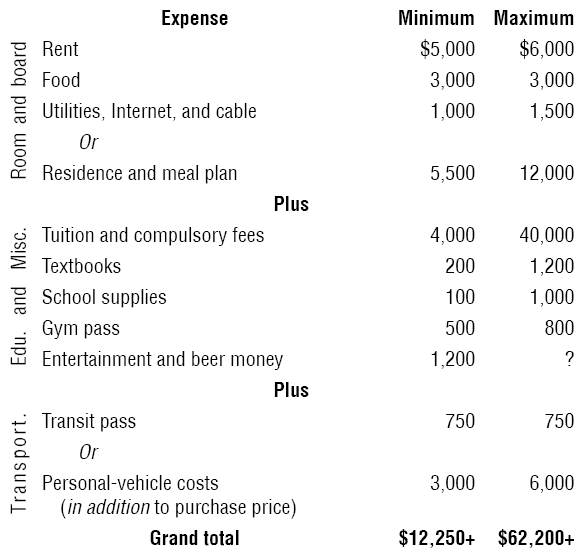

Looking for a general itemized breakdown? Here are our estimated ranges for the different categories in a typical Canadian student’s annual budget today. Remember that this doesn’t take into account one-time costs, such as a computer, furniture, and a car—and these are the costs for just one year:

As you can see, depending on a few key choices, your bottom line can differ quite a bit. For example, do your tuition and fees cost you $4,000—or $40,000? The most expensive option in the table on page 9 costs more than five times as much as the cheapest. Our personal estimate for attending one of Canada’s universities away from home and pursuing an undergraduate degree is roughly $20,000 a year—approaching $100,000 for four years. Rob Carrick, the prominent personal-finance guru for The Globe and Mail, recently quoted a similar number as he looked ahead to his eighteen-year-old son’s life after high school.

How did we get to this point in Canadian society, where everyone tells youth that they should be pursuing a post-secondary education but those same adults seem not to have many original ideas about climbing a financial mountain that grows taller every year? Well, we actually got there incrementally. While many Baby Boomers are fond of pointing out that a litre of milk and a carton of eggs also don’t cost what they did back when the Boomers were in school, the math simply doesn’t support the argument that the cost of post-secondary education has risen merely at the rate of general inflation.

A 2012 report from the Canadian Centre for Policy Alternatives shows that since 1990 the average university tuition and compulsory fees for Canadian undergraduate students have risen at an astounding rate: an average of 6.2 percent annually. Those yearly rises took place over a period when the rate of general inflation was only about one third the rate at which tuition and fees were rising. The study states that the average tuition and fees for a full course load today are $6,186 for a school year, and that number is expected to climb to a stifling $7,330 by 2015. The raw arithmetic that Mr. Carrick points to in one of his columns, titled “2012 vs. 1984: Young Adults Really Do Have It Harder Today”, shows that, if the rise in university tuition and fees had matched general inflation, the $1,000 tuition levels he enjoyed as a student in 1984 would have risen to just $2,028 today. In reality, those costs are more than three times as high.

If the costs of college and university are rising much faster than general expenses or wages, one might expect fewer Canadians to be pursuing post-secondary studies. The interesting truth is that more Canadians than ever before are attending classes after high school. Perhaps it is the nature of the new world economy, or it could be simply that today’s generation has been coached to believe that they must pursue post-secondary education no matter what. Whatever the reason, the fact is that, with more and more people paying larger and larger sums of money to obtain post-secondary credentials, something has to give. The chief candidate for what might eventually burst is the bubble that’s being inflated year after year—that of student debt. As of September 2011, there were over $22-billion in outstanding student loans in circulation: that’s roughly equivalent to the combined annual government budgets for all four Atlantic provinces! While student debt is tax-deductible, and interest rates at all-time lows have made payments easier to stomach in recent years, the drag that a large debt burden can put on our young adults is substantial and nothing to ignore.

So, what’s a student to do? Youth unemployment rates across Canada hover around fourteen percent, and consequently the battle for entry-level jobs has rarely been this desperate. Young people today realize that, in order to compete in the global marketplace, they need some kind of training after high school—but they aren’t really told how to get it or even what training might be most advantageous. Then we generally throw them to the wolves and pray that they come out with less debt than the last generation took out to buy a house. Finally, more and more of our students have grown up in environments that prize building kids’ self-esteem above all else, meaning they’re simply not prepared to deal with the financial realities of an increasingly competitive world.

Believe it or not, there is good news. By reading this book, you’re already ahead of the game and are well on your way to navigating the treacherous financial jungle young Canadians face today!

The other news you should find encouraging is that attending post-secondary schooling is still generally a great deal, even though costs are skyrocketing. The financial benefits of attaining a college diploma or a university degree are well documented. Paul Davidson, President of the Association of Universities and Colleges of Canada, has highlighted census information showing the average lifetime earnings of someone with an undergraduate degree will be about $1.4-million more than those of someone without a post-secondary degree. Even the average college graduate’s lifetime earnings will be about $400,000 more than those of the person without a post-secondary degree. We are a little dubious as to how large the gap is between college diplomas and university degrees in that information, but the principle that a post-secondary education still holds a lot of value is consistent across every study we’ve read. Davidson goes on to say that, since the economic shakedown that began in 2008, there have been more than 300,000 new jobs created for university graduates—and there’s been a loss of 430,000 jobs for those without post-secondary education. With the disappearance of so many blue-collar manufacturing jobs, there’s little doubt we’re moving quickly to a more information-based economy—and this will largely benefit certain types of post-secondary education, regardless of the initial cost of that education.

While there is no denying the fact that students today face an uphill battle, it is not exactly Mission: Impossible to get your degree while you keep your overall debt figure low. It will require some tough choices and a little bit of effort in order to get your financial house in order, but the juice is definitely worth the squeeze. Many students stumble through their late teens and early twenties in some sort of student-loan-fuelled, lifestyle-inflating haze. They believe that a budget is more confusing than advanced calculus, and debt becomes some imaginary concept to be dealt with in a faraway land called “The Future”. If you can manage to learn and execute a few key tips found within these pages, they can make a substantial difference in your getting out of school on good financial terms and in keeping you out of the “Look at How Much Student Debt I Have” features that newspapers love so much these days.

Chapter 1 Summary

- A post-secondary education costs a lot of money—especially if you decide to move out of your parents’ place to attend school (roughly $20,000 per year in that case).

- Tuition is rising at a rate much quicker than that of general inflation. This means that school is likely to take up an ever growing portion of the average personal or family budget as the years go by.

- Canadian students are taking on more debt than ever before, and the amount they owe is increasing rapidly.

- A post-secondary education is still an excellent investment, and will stay that way in an information-based economy.

Oh, and don't forget about our giveaway this week! What's the point of writing a book if you can't be a little vain and give away a few FREE copies right? In addition to wanting to reward our loyal readers, we are obviously trying to maximize our modest marketing budget and are asking for your help in spreading the word about this great new resource.

To qualify for our draw, simply fill out the form below and then set about getting as many entries as you can.

a Rafflecopter giveaway

I know the reason I was able to graduate with minimal debt after university was because I worked part-time and lived with my parents. I definitely would encourage anyone to do the same if they are able to because it’s a great feeling not having to pay back $50,000 after you get your diploma!

FYI, if you are taking engineering at a top tier school, you could pay $65,000+ in tuition over four years.

Good to know Mom!